Independent dental insurance is a self-purchased policy that helps cover clinical dental care, ranging from preventive cleanings to major restorative procedures like implants. These plans typically involve monthly premiums, annual maximums, and specific waiting periods for complex surgical interventions. Understanding how to navigate these policies can significantly reduce out-of-pocket expenses for comprehensive oral rehabilitation.

Clinical Summary:

Navigating independent dental insurance requires a thorough understanding of clinical coding, coverage tiers, and policy limitations. While these self-funded plans excel at covering preventive diagnostics, major surgical procedures such as implantology often face strict waiting periods, missing tooth clauses, and annual maximum caps. Clinicians must meticulously document medical necessity through radiographic evidence and periodontal charting to secure pre-treatment estimates. For patients requiring extensive full-mouth rehabilitation, strategically staging treatments across multiple benefit periods or utilizing out-of-network benefits for high-quality international care can optimize financial resources while supporting favorable biological outcomes.

Key Takeaways:

- Independent dental insurance is purchased directly by the patient, separate from employer-sponsored group plans.

- Major restorative procedures typically require a 6 to 12-month waiting period before coverage activates.

- Insurance rarely covers the surgical placement of the implant fixture, often only contributing to the final prosthetic crown.

- Detailed clinical documentation, including CBCT scans and narrative reports, is essential for claim approval.

- Out-of-network benefits can often be applied to treatments performed at certified international clinics.

Understanding Independent Dental Insurance for Major Clinical Procedures

Independent dental insurance provides self-funded coverage for oral healthcare, categorized into preventive, basic, and major clinical services. Understanding network types like PPO or HMO is crucial for accessing specialized surgical care.

When patients transition away from employer-sponsored healthcare, securing independent dental insurance becomes a critical step in maintaining long-term oral health. Unlike group policies negotiated by corporate HR departments, independent plans are selected and funded entirely by the individual or family. From a clinical perspective, the structure of these plans directly influences treatment sequencing, diagnostic workflows, and the choice of restorative materials. The primary distinction among these policies lies in their network structure, which dictates a patient’s freedom to choose their preferred clinical specialist.

Preferred Provider Organization (PPO) plans are the most common and clinically flexible type of independent dental insurance. A PPO allows patients to visit any licensed dentist, though financial incentives are provided for utilizing in-network providers. For complex surgical procedures, this flexibility is paramount. It allows patients to seek out highly specialized oral surgeons or prosthodontists rather than being restricted to a narrow list of general practitioners. Health Maintenance Organization (HMO) plans, conversely, require patients to select a primary care dentist who acts as a gatekeeper, managing all referrals to specialists. While HMOs typically feature lower premiums and no annual maximums, the restricted network can be a significant barrier when seeking advanced reconstructive care[1].

Dr. Nguyen Van Cuong, a leading specialist in restorative dentistry, frequently emphasizes to patients that insurance coverage does not always dictate clinical necessity. He advises that while a procedure may be biologically imperative to prevent further oral degradation, it might still be classified as “elective” or “non-covered” by an independent policy. To bridge this gap, comprehensive diagnostic imaging and detailed clinical narratives are essential tools his team uses to advocate for maximum patient coverage.

Furthermore, independent dental insurance policies are universally structured around an annual maximum—the absolute highest dollar amount the insurer will pay toward clinical care within a benefit year. Once this threshold is reached, the patient assumes full financial responsibility for any subsequent treatments. Understanding this limitation is vital when planning multi-disciplinary cases, as the cost of a single surgical intervention can easily exhaust a standard annual maximum.

How Independent Plans Cover Dental Implants and Restorations

Most independent policies classify implantology as a major restorative service, typically covering a percentage of the crown or abutment while excluding the surgical fixture placement.

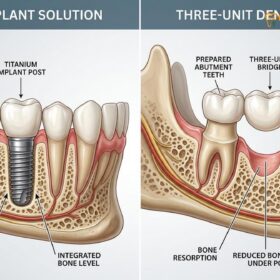

The intersection of independent dental insurance and modern implantology is often a source of confusion for patients. Historically, insurance carriers viewed implants as an elective luxury, heavily favoring traditional removable dentures or tooth-supported bridges. However, as the clinical consensus has firmly established implants as the standard of care for edentulism—due to their ability to preserve alveolar bone and restore natural occlusal forces—insurance models have slowly adapted. Despite this progress, coverage remains highly fragmented and heavily regulated by policy stipulations[2].

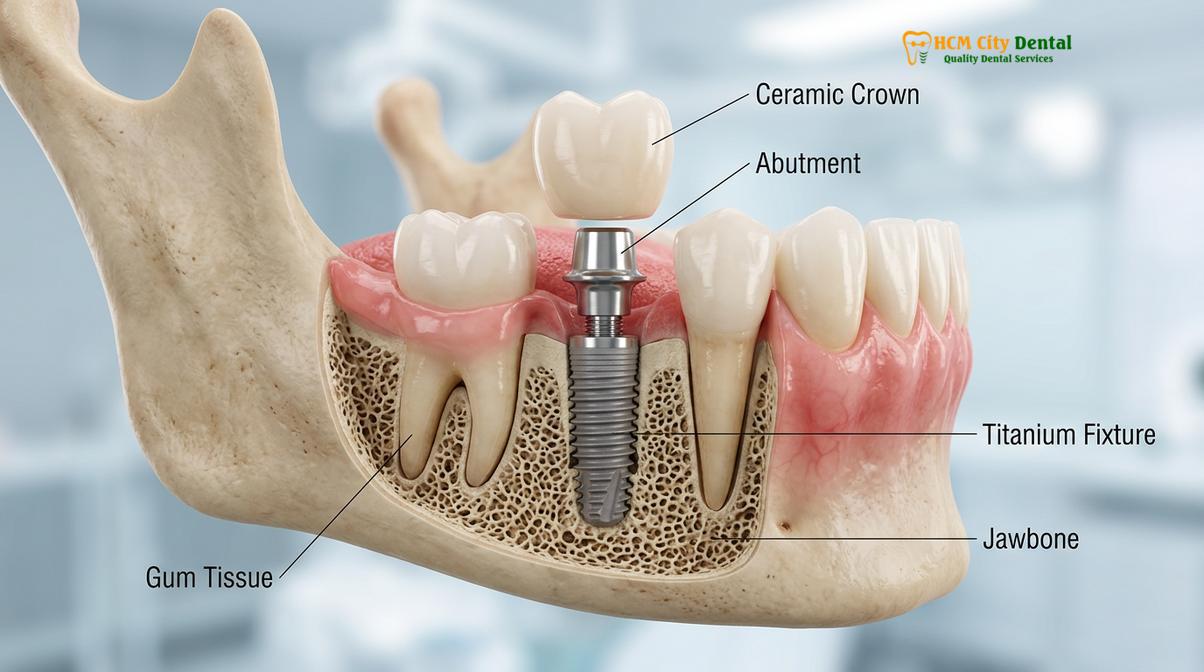

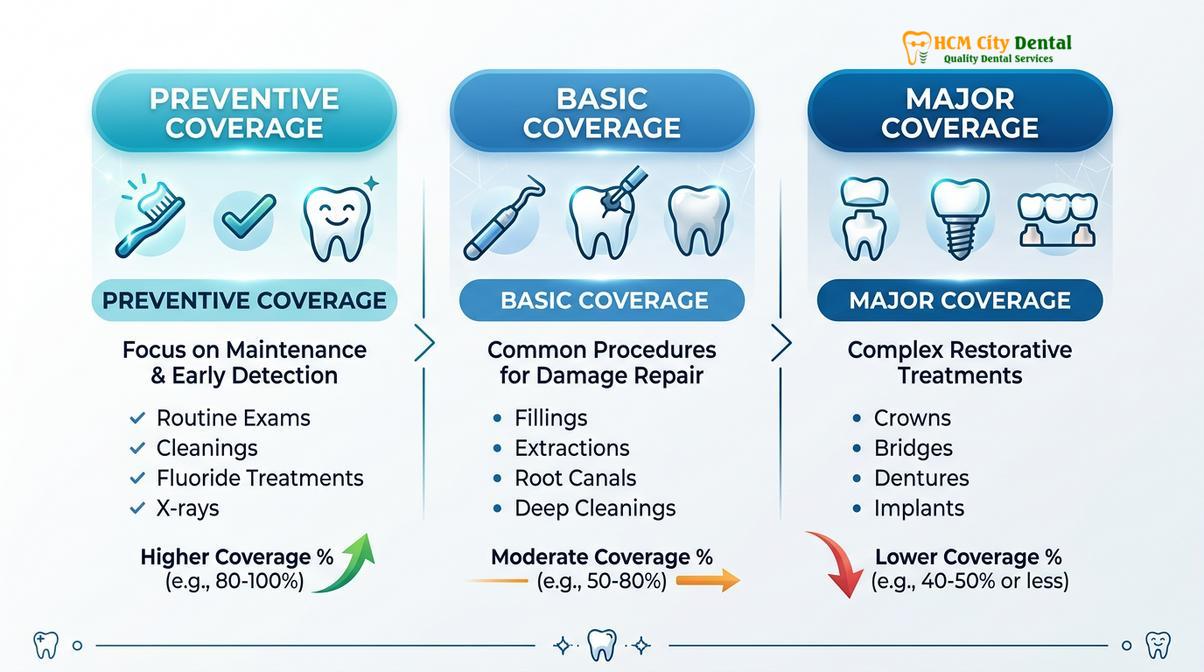

To understand how insurance processes these claims, one must break down the procedure into its three distinct clinical components: the surgical fixture (the titanium root embedded in the bone), the abutment (the connector), and the final prosthetic crown. Most independent dental insurance plans utilize a 100-80-50 coverage structure. Preventive care is covered at 100%, basic restorative work (like fillings) at 80%, and major restorative work at 50%. Implants fall squarely into the major category.

However, a critical caveat exists: many policies will only apply that 50% coverage to the final Dental Implants restoration (the crown) and the abutment, explicitly excluding the surgical placement of the titanium fixture itself. The rationale provided by insurers is often that alternative, less expensive treatments are available to restore basic masticatory function. Clinicians argue against this, noting that removable prosthetics can accelerate bone resorption, but insurance guidelines are driven by actuarial tables rather than optimal biological outcomes.

| Service Category | Clinical Examples | Typical Coverage Rate | Standard Waiting Period |

|---|---|---|---|

| Preventive / Diagnostic | Comprehensive Exams, Digital X-rays, Prophylaxis | 100% | None |

| Basic Restorative | Composite Fillings, Simple Extractions, Periodontal Scaling | 70% – 80% | 0 – 6 Months |

| Major Restorative | Crowns, Bridges, Endodontics, Dentures | 50% | 6 – 12 Months |

| Implantology | Surgical Placement, Bone Grafting, Abutments | 0% – 50% (Highly Variable) | 12 – 18 Months |

Another significant hurdle is the “missing tooth clause.” This is a common stipulation in independent dental insurance contracts stating that the policy will not cover the replacement of a tooth that was extracted before the policy’s effective date. If a patient lost a molar previously and recently purchased an independent plan to help pay for an implant, the missing tooth clause will likely trigger an automatic denial of the claim. Clinicians must carefully review a patient’s dental history and insurance contract before estimating coverage amounts.

Navigating Waiting Periods and Pre-Treatment Estimates

Waiting periods mandate a specific timeframe before major clinical coverage activates, requiring dentists to submit detailed pre-treatment estimates with radiographic evidence to verify medical necessity.

One of the most defining characteristics of independent dental insurance, as opposed to employer-sponsored group plans, is the strict enforcement of waiting periods. Because individuals can purchase these plans at any time, insurance companies implement waiting periods to prevent adverse selection—the practice of a patient buying a policy solely to cover an immediate, expensive surgical need and then canceling the policy shortly after. For major clinical procedures, this waiting period is typically 12 months, though some premium plans may reduce it to 6 months.

From a clinical standpoint, waiting periods present a significant challenge. Dental pathology is progressive. A tooth that requires a standard crown today may deteriorate into requiring endodontic therapy or extraction if treatment is delayed for a year to satisfy an insurance requirement. Clinicians must carefully balance the patient’s financial constraints with the biological urgency of the condition. In cases of active infection or rapid structural decay, delaying care is contraindicated, regardless of insurance status.

To provide financial clarity before initiating complex care, the standard clinical workflow involves submitting a pre-treatment estimate (also known as a pre-determination of benefits) to the insurance carrier. This is not a guarantee of payment, but rather a formal review by the insurer’s dental consultants to determine how the proposed treatment aligns with the patient’s specific policy guidelines[3].

“A pre-treatment estimate is an essential communication tool between the clinic, the patient, and the insurer. By submitting comprehensive 3D imaging, periodontal charting, and a detailed narrative of medical necessity, we eliminate financial surprises and allow the patient to make fully informed decisions about their reconstructive care.”

The documentation required for a successful pre-treatment estimate for implantology is extensive. The clinical team must provide current periapical and panoramic radiographs, and increasingly, Cone Beam Computed Tomography (CBCT) scans. A written narrative must explain why alternative treatments are clinically inappropriate. Once the estimate is returned, the patient and the financial coordinator can review the exact out-of-pocket responsibilities and discuss how long the dental implant procedure takes to properly sequence the appointments.

Utilizing Independent Insurance for Treatment Abroad in Ho Chi Minh City

Many independent PPO plans offer out-of-network benefits that can be applied to international dental care, allowing patients to combine insurance reimbursements with lower overseas treatment costs.

As the cost of complex dental rehabilitation continues to rise in Western countries, a growing number of patients are exploring cross-border care. A common misconception is that independent dental insurance is entirely useless outside of the patient’s home country. In reality, many PPO policies include out-of-network benefits that can be utilized globally, provided the international clinic meets specific credentialing and documentation standards[5].

When a patient travels to a facility for international care, the financial workflow shifts from a direct-billing model to a reimbursement model. Because international clinics are not contracted directly with foreign insurance carriers, the patient is responsible for paying the clinic directly at the time of service. Following the completion of the clinical procedures, the dental office provides the patient with a comprehensive, itemized receipt translated into English, complete with the corresponding international CDT codes, tooth numbers, and surface designations.

Clinical Case Study: International Insurance Utilization

Patient Profile: A 52-year-old patient requiring bilateral posterior restorations traveled to HCMC Dental Clinic in Ho Chi Minh City.

Clinical Workflow: The patient utilized their independent PPO insurance domestically to cover the initial diagnostic CBCT scans and preventive cleanings at 100%. Upon arriving in Vietnam, the surgical placement and prosthetic loading were completed at a fraction of the domestic cost.

Insurance Outcome: The clinic provided an itemized superbill with standardized CDT codes. The patient submitted this to their insurer and received a 50% out-of-network reimbursement for the prosthetic crowns, effectively combining the lower international clinical fees with their insurance benefits for maximum financial efficiency.

This hybrid approach requires meticulous clinical documentation. Insurers will heavily scrutinize international claims to ensure compliance. Therefore, the provision of high-resolution pre-operative and post-operative radiographs is non-negotiable. The clinical team must ensure that the quality of the documentation matches or exceeds the standards expected by domestic insurance auditors. Patients considering this route should also verify if their policy requires pre-authorization for out-of-network international care prior to booking their travel.

Furthermore, patients must consider the long-term maintenance of their restorations. High-quality international clinics provide comprehensive documentation that the patient can take back to their local dentist for ongoing hygiene and monitoring. Understanding the nuances of a dental implant warranty and how it interacts with routine insurance-covered cleanings ensures the longevity of the surgical investment. For patients requiring multiple dental implants, the combination of international fee structures and out-of-network insurance reimbursement often makes comprehensive rehabilitation financially accessible.

Clinical Considerations: Maximizing Your Annual Maximum

Strategic clinical planning allows patients to split complex, multi-stage treatments across two benefit periods, effectively doubling the available insurance payout for extensive reconstructive procedures.

The annual maximum is the most restrictive element of independent dental insurance when dealing with major clinical procedures. Most plans cap their annual payout between a set limit. Given that a single comprehensive implant restoration can easily exceed this amount, patients often find their benefits exhausted before the treatment is even completed. However, because implantology is inherently a multi-stage process that requires months of biological healing, clinicians can strategically sequence the treatment to span across two different insurance benefit years[4].

This strategy, known as “staging,” requires precise clinical timing. For example, if a patient’s insurance plan resets on January 1st, the surgical placement of the titanium fixture and any necessary alveolar bone grafting can be performed late in the year. The cost of this initial surgical phase will be applied to the current year’s annual maximum. The patient then undergoes the mandatory osseointegration period, during which the bone biologically fuses to the implant surface.

Once osseointegration is confirmed via radiographic evaluation in the new year, the restorative phase—involving the abutment and the final ceramic crown—can commence. Because the new benefit year has started, the patient has a fresh annual maximum to apply toward these prosthetic costs. This staging approach is particularly beneficial for patients wondering if they can get dental implants with bone loss, as the preliminary grafting procedures can be billed in one year, while the implant placement and restoration are billed in the next.

Important Clinical Notes: When to Consult Your Dentist

Regular monitoring and professional maintenance are critical for the long-term success of implant restorations, regardless of insurance coverage limitations.

While independent dental insurance can help offset the initial costs of restorative care, the long-term viability of an implant depends heavily on patient compliance and routine clinical monitoring. Patients should not delay necessary maintenance simply because their annual insurance maximum has been reached. Early intervention is always more conservative and cost-effective than treating advanced complications.

According to guidelines established by the Vietnam Odonto-Stomatology Association (VOSA) regarding implantology standards, patients should seek immediate clinical evaluation if they experience persistent discomfort, localized swelling, or bleeding around an implant site[6]. These symptoms may indicate the onset of peri-implant mucositis or, more severely, peri-implantitis—an inflammatory condition affecting the soft and hard tissues surrounding the fixture. Understanding proper peri-implantitis prevention protocols is essential for protecting your surgical investment.

“Proactive maintenance is the cornerstone of implant dentistry. We encourage patients to view their independent dental insurance as a tool for preventive care rather than just a safety net for major surgeries. Regular professional cleanings and radiographic monitoring are vital for ensuring the surrounding bone and gingival tissues remain healthy.”

Patients should schedule professional evaluations at least twice a year. During these visits, the clinician will assess the occlusal forces on the implant crown, evaluate the integrity of the abutment connection, and measure the probing depths around the peri-implant tissues. If any signs of bone loss or mechanical loosening are detected, prompt clinical action can often resolve the issue before it compromises the entire restoration.

Conclusion & Next Steps

Navigating independent dental insurance requires careful planning, but leveraging out-of-network benefits for international care can provide a highly effective solution for complex dental needs.

Understanding the intricacies of independent dental insurance—from waiting periods and missing tooth clauses to annual maximums and CDT coding—empowers patients to make informed decisions about their oral healthcare. While domestic coverage for major surgical procedures like implants is often limited, strategic treatment staging and the utilization of out-of-network benefits can significantly reduce out-of-pocket expenses.

For those requiring extensive reconstructive work, combining insurance reimbursements with the high-quality, cost-effective care available at HCMC Dental Clinic in Ho Chi Minh City offers a compelling pathway to restoring optimal oral function and aesthetics. By working closely with experienced clinical coordinators, patients can navigate the complexities of international claims and achieve lasting results. To explore how international care compares to domestic options, review our detailed guide on dental implant costs in Vietnam vs Australia and take the first step toward your comprehensive smile restoration today.

References

- Journal of the American Dental Association. The economic impact of dental insurance on implant therapy utilization.

- International Journal of Oral and Maxillofacial Implants. Clinical outcomes and cost-effectiveness of implant-supported restorations.

- Journal of Periodontology. Alveolar ridge preservation and insurance coding classifications.

- Clinical Oral Implants Research. Patient-reported outcomes and financial barriers in comprehensive implant dentistry.

- British Dental Journal. Navigating out-of-network dental benefits for international clinical care.

- Vietnam Odonto-Stomatology Association (VOSA). Guidelines on implantology standards and international patient care.